TFSA Annual Contribution Limits: Maximizing Your Savings Potential

Share

Tax-Free Savings Accounts (TFSAs) are a cornerstone of financial planning for Canadians, offering unparalleled flexibility and tax advantages. However, to fully leverage their benefits, it’s essential to understand how TFSA annual contribution limits work. Misunderstanding these limits can lead to missed opportunities or penalties, so staying informed is key.

In this guide, we’ll explore everything you need to know about TFSA contribution limits, from annual limits and unused room to penalties and strategic tips for maximizing your savings.

What is a TFSA?

Introduced in 2009, the Tax-Free Savings Account is a registered account designed to help Canadians grow their savings tax-free. Any income earned within a TFSA—whether from interest, dividends, or capital gains—is entirely tax-free, and withdrawals are not subject to taxes.

Eligible investments for TFSAs include:

Guaranteed Investment Certificates (GICs).

Stocks.

Mutual funds.

Bonds.

Exchange-Traded Funds (ETFs).

This flexibility makes TFSAs an excellent tool for short-term goals, retirement savings, or emergency funds.

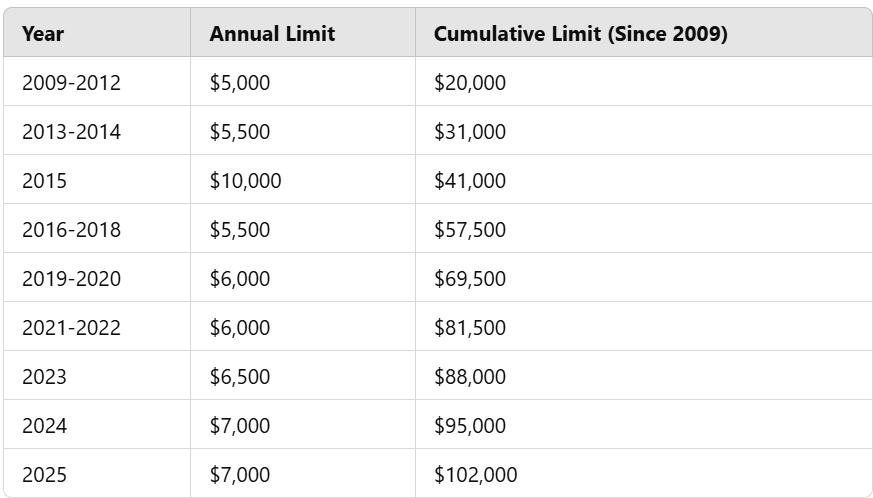

Annual Contribution Limits: A Year-by-Year Breakdown

Each year, the Canada Revenue Agency (CRA) sets a contribution limit for TFSAs. For 2025, the TFSA contribution limit is $7,000. These annual limits are cumulative, meaning unused contribution room carries forward to future years.

Here’s a year-by-year breakdown of TFSA limits since their inception :For individuals who have been eligible to contribute since 2009 and have never deposited funds, the lifetime contribution room as of 2025 is $101,000.

Carry-Forward Rules: Making the Most of Unused Contribution Room

One of the most significant advantages of TFSAs is the ability to carry forward unused contribution room indefinitely. For example, if you were eligible to contribute $6,000 in 2023 but only deposited $3,000, the remaining $3,000 would carry forward to 2024, adding to your annual limit.

How to Calculate Your Contribution Room

To determine your total available contribution space:

Start with the cumulative limit for the current year.

Subtract all prior contributions.

Add any withdrawals made in the previous year (which are added back to your room the following year).

What Happens If You Over-Contribute?

Exceeding your TFSA contribution limit can result in penalties. The CRA imposes a 1% monthly tax on the excess amount until it is withdrawn or your contribution room increases in the following year.

Steps to Correct an Over-Contribution

Determine the excess amount.

Withdraw the over-contributed funds immediately to minimize penalties.

Notify the CRA if you’re unsure of your current contribution status.

Tracking contributions across multiple TFSAs is critical to avoid this scenario. Keeping a record of deposits and withdrawals can save you from costly mistakes.

Common Misconceptions About TFSA Contributions

1. Contribution Room Does Not Reset After Withdrawals

Many people mistakenly believe that withdrawing funds immediately frees up contribution space in the same year. In reality, the withdrawn amount is added back to your contribution room only in the following calendar year.

2. Contributions Aren’t Based on Income

Unlike RRSPs, TFSA contribution room is not tied to your income. Every eligible Canadian over the age of 18 receives the same annual limit.

3. Multiple Accounts Share One Limit

You can open multiple TFSAs at different institutions, but the contribution limit applies across all accounts. Contributions to multiple accounts must be tracked to avoid exceeding the overall limit.

Tips to Maximize Your TFSA Contributions

Set Up Automatic Contributions Automating your contributions ensures consistency and helps you stay within your limit.

Align Investments with Your Goals For short-term goals, consider low-risk options like GICs or high-interest savings. For long-term growth, higher-risk investments like equities may be suitable.

Prioritize TFSA Contributions Maximizing your TFSA before contributing to taxable accounts ensures you’re taking full advantage of tax-free growth.

Track Contributions Carefully Use online tools or consult with a financial advisor to monitor your TFSA activity.

The Role of Financial Advisors in TFSA Planning

Understanding TFSA rules and contribution limits can be complex. Financial advisors play a critical role in helping you:

Optimize your contribution strategy.

Align TFSA investments with your broader financial goals.

Avoid common pitfalls, such as over-contributing or mismanaging investments.

At Dunbrook Associates, we specialize in creating tailored financial plans to help clients maximize their TFSA benefits. Whether you’re saving for retirement, a major purchase, or an emergency fund, our expertise ensures you’re making the most of your tax-free savings.

TFSAs offer incredible advantages, but understanding the annual contribution limits is essential to unlocking their full potential. By staying informed, tracking your contributions, and consulting with financial professionals, you can avoid costly mistakes and achieve your financial goals faster.

Ready to make the most of your TFSA? Contact Dunbrook Associates today for personalized advice tailored to your unique needs.

Need Personalized Support?

Our team is committed to clarity, precision, and long-term guidance.

When building an investment portfolio, one of the most important decisions is whether to focus primarily on growth, income, or a combination of the two. Both growth investing and income investing can play a valuable role in a long-term financial plan, but they are designed to meet different needs.

Whether you're just beginning your financial journey or approaching retirement, developing strong financial habits today can significantly improve your financial future. The good news is that these habits don't require perfection they simply require consistency.

While an inheritance can provide financial security and new opportunities, making thoughtful decisions is essential to ensure those assets continue to benefit you and future generations.

July 13, 2026

Cookie Settings

We use cookies to enhance your browsing experience, serve personalised ads or content, and analyse our traffic. By clicking "Accept All", you consent to our use of cookies.