Common Retirement Planning Mistakes and How to Avoid Them

Share

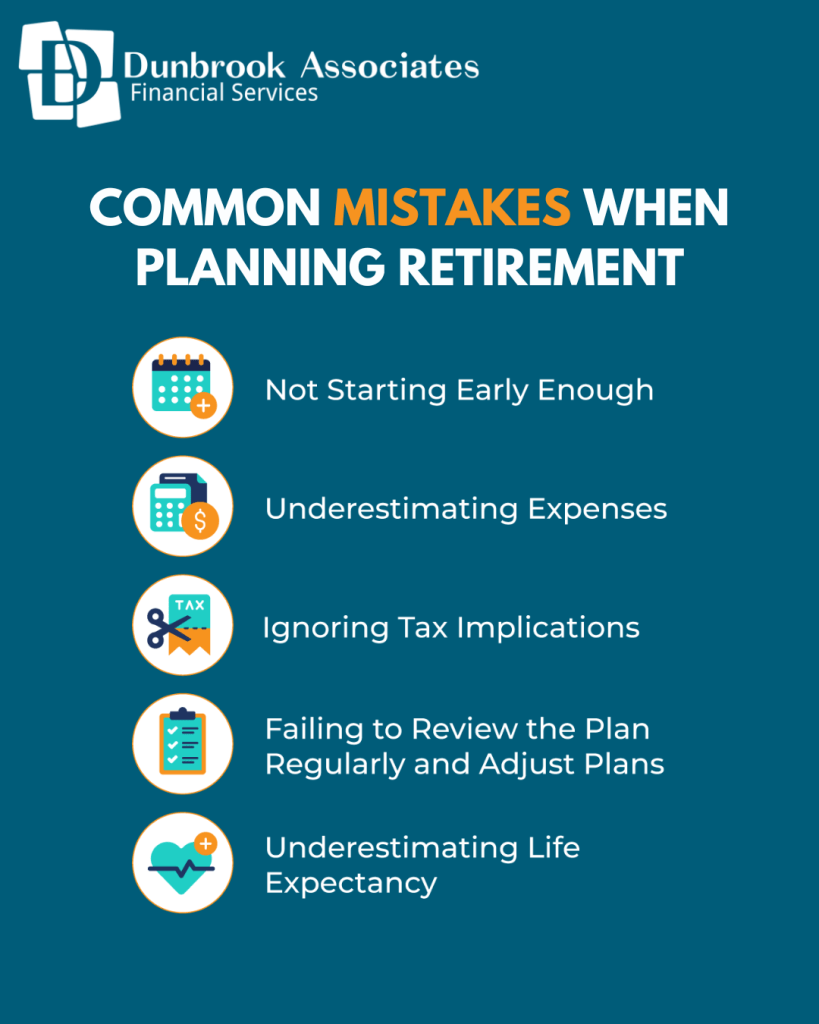

Retirement is a significant milestone that many of us look forward to, but planning for it requires careful consideration. Mistakes in retirement planning can have long-lasting impacts on your financial security. In this blog, we’ll explore some of the most common retirement planning mistakes and offer tips on how to avoid them.

Not Starting to Save Early Enough

Delaying your retirement savings can lead to major shortfalls later in life. The earlier you start saving, the more time your investments have to grow through the power of compound interest. Unfortunately, many people wait too long to begin.

Why it happens: Life gets in the way—mortgages, student loans, and daily expenses often take priority over long-term savings.

How to avoid it: Start saving for retirement as early as possible. Even small amounts invested in your 20s and 30s can grow significantly over time. Maximize contributions to accounts like RRSPs, TFSAs (for Canadians), or other tax-advantaged accounts

Underestimating Retirement Expenses

One of the most prevalent mistakes in retirement planning is underestimating how much money you’ll need. Many people assume that their expenses will drastically reduce after retirement. However, retirement comes with its own set of expenses such as healthcare, travel, hobbies, and long-term care, that could add up quickly.

Why it happens: People often base future projections on their current lifestyle, forgetting inflation and future healthcare needs.

How to avoid it: Create a realistic retirement budget that takes these expenses into account. Factor in inflation and rising healthcare costs, and aim to save more than you think you’ll need to cover unanticipated costs.

Failing to Plan for Taxes in Retirement

Many retirees overlook the tax implications of their income sources. Distributions from traditional RRSP’s and Company Pensions are taxable, and failing to plan for this can result in an unexpectedly high tax bill.

Why it happens: People assume they’ll be in a lower tax bracket after retirement or don’t fully understand how taxes on different accounts work.

How to avoid it: Consider the tax characteristics of your investments and retirement accounts. Tax-Free Saving Accounts, for example, offer tax-free withdrawals in retirement, which can provide significant tax relief. Work with your advisor to plan strategically and minimize taxes.

Poor Investment Choices Near Retirement

As you near retirement, making overly aggressive or overly conservative investment choices can hurt your retirement portfolio. Being too aggressive could lead to significant losses, while being too conservative may not provide enough growth to cover your retirement years.

Why it happens: People either panic due to market volatility or feel overly confident in continued market growth.

How to avoid it: Maintain a balanced portfolio that includes a mix of stocks, bonds, and other assets. Adjust your investment strategy as you near retirement to reduce risk while still allowing for growth. Consult with your financial advisor to tailor your investment strategy to your specific timeline and goals.

Not Diversifying Investments

Relying too much on one type of asset, whether it's stocks, real estate, or a single investment account, can be risky. Lack of diversification makes your portfolio vulnerable to market volatility and economic downturns.

Why it happens: Many investors stick to what they know and are comfortable with, or they chase recent high-performing assets.

How to avoid it: Diversify across asset classes, industries, and geographical locations. A well-balanced portfolio with a variety of investment types can better weather market fluctuations.

Forgetting to Update Estate Plans

Your estate plan should be part of your overall retirement strategy. Failing to update your will, trusts, and beneficiary designations can create complications for your heirs.

Why it happens: Life changes—like marriage, divorce, births, and deaths—are often not reflected in outdated estate plans.

How to avoid it: Regularly review and update your estate plan as your family situation and financial status change. Ensure your beneficiary designations are current on all retirement and investment accounts.

Overlooking Inflation

Inflation can significantly reduce the purchasing power of your retirement savings. If you fail to account for inflation, you could find yourself with a much lower standard of living than expected in retirement.

Why it happens: People often focus on nominal figures rather than inflation-adjusted projections.

How to avoid it: When planning, factor in a reasonable inflation rate (typically around 2-3%). Include investments like stocks, which tend to outpace inflation over time, and regularly review your retirement plan to adjust for inflationary changes.

Retiring Too Early

Many people dream of retiring early, but doing so without sufficient financial preparation can cause significant strain on your retirement savings. Early retirement means more years of living expenses and fewer years of saving and earning compound interest.

Why it happens: The allure of early retirement can make people overestimate their readiness or underestimate future costs.

How to avoid it: Before deciding to retire early, carefully evaluate your financial situation. Consult with your financial advisor to ensure you won’t outlive your savings.

Withdrawing Too Much Too Soon

Drawing too much from your retirement accounts early on can deplete your savings faster than anticipated, leaving you with insufficient funds later in life.

Why it happens: People underestimate how long they’ll live or fail to budget their withdrawals effectively.

How to avoid it: Follow the 4% rule as a guideline, which suggests withdrawing no more than 4% of your retirement savings each year. This can help ensure that your savings last for the duration of your retirement. Periodically revisit your withdrawal strategy to account for changing market conditions.

Not Consulting a Financial Advisor

Do-it-yourself (DIY) retirement planning can be risky, especially when navigating the complexities of taxes, investments, and estate planning. Without professional guidance, you may overlook critical aspects of retirement planning.

Why it happens: Some people try to save on advisory fees, or they believe they can handle their finances on their own.

How to avoid it: A professional financial advisor can help you avoid costly mistakes and create a retirement plan tailored to your specific needs. Dunbrook Financial Advisors will help guide you through the process, offering personalized advice to secure your financial future.

Avoiding these common retirement planning mistakes can significantly enhance your financial security during retirement. By starting early, diversifying your investments, and consulting with financial professional at Dunbrook Associates, you can ensure that you’re on the right track for a comfortable retirement. Keep in mind that retirement planning is not a one-time task but an ongoing process that requires regular adjustments as your circumstances and the economic environment change.

Need Personalized Support?

Our team is committed to clarity, precision, and long-term guidance.

When building an investment portfolio, one of the most important decisions is whether to focus primarily on growth, income, or a combination of the two. Both growth investing and income investing can play a valuable role in a long-term financial plan, but they are designed to meet different needs.

Whether you're just beginning your financial journey or approaching retirement, developing strong financial habits today can significantly improve your financial future. The good news is that these habits don't require perfection they simply require consistency.

While an inheritance can provide financial security and new opportunities, making thoughtful decisions is essential to ensure those assets continue to benefit you and future generations.

July 13, 2026

Cookie Settings

We use cookies to enhance your browsing experience, serve personalised ads or content, and analyse our traffic. By clicking "Accept All", you consent to our use of cookies.