Understanding Management Expense Ratios (MERs): A Guide for Investors

Share

Investing is a cornerstone of building wealth, and understanding the costs associated with investments is crucial for making informed decisions. Among these costs, Management Expense Ratios (MERs) play a pivotal role in determining the overall performance of an investment. This guide will delve into what MERs are, how they impact investments, and why understanding them is vital for achieving your financial goals.

What Are Management Expense Ratios (MERs)?

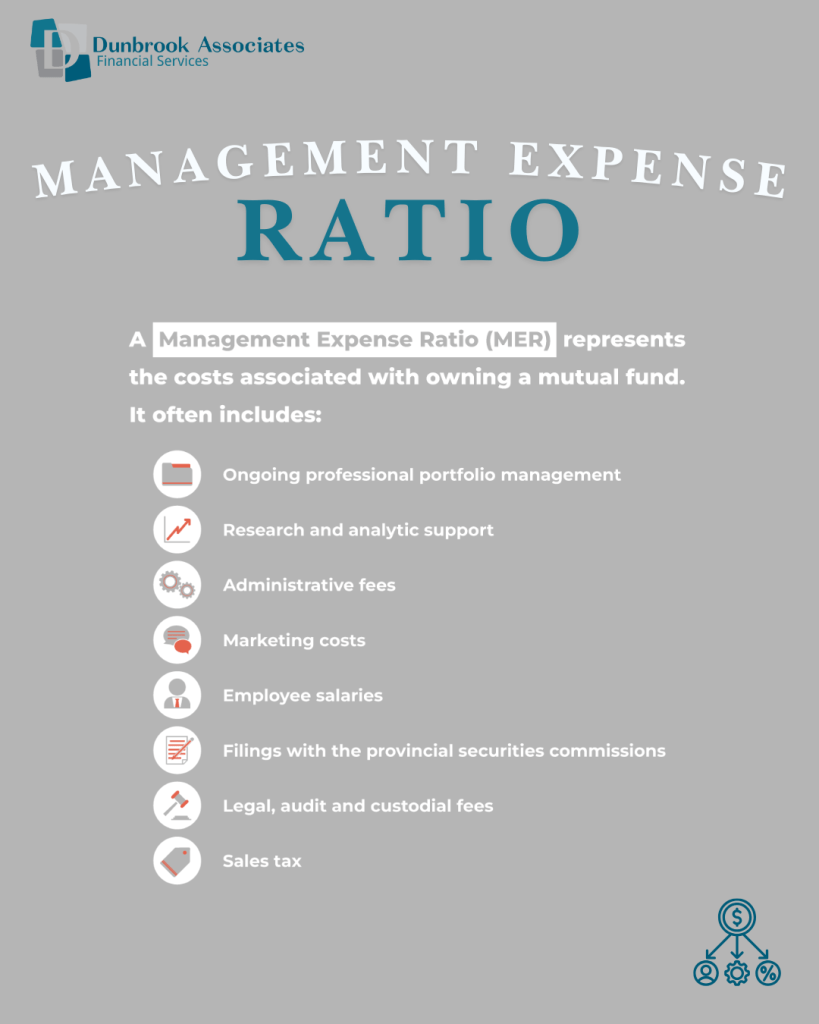

The Management Expense Ratio (MER) represents the annual cost of managing an investment fund, expressed as a percentage of the fund's assets. It is a key metric used to evaluate the cost-efficiency of mutual funds, exchange-traded funds (ETFs), and other managed investment products.

MERs typically include:

Management Fees: Paid to fund managers for their expertise and oversight.

Operating Expenses: Administrative costs, such as legal, accounting, and regulatory fees.

Taxes: In some regions, taxes like GST or HST are included.

For example, if a fund has an MER of 2% and you invest $10,000, you will pay $200 annually in fees, regardless of the fund's performance.

Breaking Down the Components of MERs

To understand the implications of MERs, it's essential to examine their components in detail:

1. Management Fees

These are the largest portion of the MER, compensating fund managers for their expertise in selecting and managing investments. Active funds, which require hands-on management, typically have higher management fees than passive funds like index ETFs.

2. Administrative Costs

Operating a fund involves various administrative tasks, including maintaining records, regulatory compliance, and shareholder communications. These costs are bundled into the MER.

3. Performance-Based Fees

Some funds charge additional fees based on their performance relative to a benchmark. While not always included in the MER, they can add to the overall cost.

Why Do MERs Matter?

MERs directly impact your investment returns. Over time, even a small percentage difference can significantly affect your portfolio's growth due to the power of compounding. Consider this example:

Fund A: MER of 2%

Fund B: MER of 0.5%

If both funds earn a gross annual return of 8%, the net return for Fund A will be 6% (8% - 2%), while Fund B will earn 7.5% (8% - 0.5%). Over 20 years, this seemingly small difference can lead to a substantial gap in investment outcomes.

Types of Investment Products and Their MERs

Different investment products have varying MERs, reflecting the level of management and complexity involved:

1. Mutual Funds

Mutual funds often have higher MERs due to active management and associated operating costs. The average MER for mutual funds ranges from 1.5% to 2.5%.

2. Exchange-Traded Funds (ETFs)

ETFs are known for their low costs, with MERs typically between 0.05% and 0.75%. Most ETFs follow a passive strategy, tracking an index rather than relying on active management.

3. Index Funds

Index funds, like ETFs, have lower MERs, making them attractive for cost-conscious investors seeking broad market exposure.

4. Segregated Funds

Offered by insurance companies, segregated funds often have higher MERs (2% to 3%) due to added features like maturity guarantees and estate benefits.

How to Evaluate MERs

When assessing investment options, MERs should be considered alongside other factors like performance, risk, and your financial goals. Here’s how you can evaluate MERs effectively:

1. Compare Similar Funds

Compare the MERs of funds within the same category. For instance, evaluate mutual funds against other mutual funds or ETFs against ETFs.

2. Understand Value for Cost

Higher MERs may be justified if the fund consistently outperforms its peers or offers unique benefits. However, if similar funds provide comparable returns at a lower cost, it might be wise to switch.

3. Review Historical Returns

Ensure that a fund’s performance justifies its MER. Look at long-term returns to assess whether the cost aligns with the benefits.

Strategies to Minimize MER Impact

Investors can employ various strategies to reduce the impact of MERs on their portfolios:

1. Opt for Low-Cost Funds

Consider low-cost ETFs or index funds, which often have MERs below 0.5%.

2. Monitor Portfolio Turnover

Funds with high turnover rates may incur additional trading costs, indirectly affecting returns. Low-turnover funds generally have lower MERs.

3. Use a Fee-Based Advisor

A fee-based financial advisor charges a flat fee or percentage of assets rather than commissions, helping you select cost-effective investments.

Common Misconceptions About MERs

1. Higher MERs Mean Better Performance

While higher MERs may indicate active management, they don’t guarantee superior returns. In fact, many high-cost funds underperform their benchmarks after fees.

2. MERs Cover All Costs

MERs don’t include trading costs or sales charges like front-end or back-end loads. These additional expenses can further erode returns.

3. MERs Are Fixed

MERs can change over time. It’s essential to review fund documents regularly to stay informed.

MERs and Your Financial Plan

MERs should align with your broader financial strategy. For long-term goals like retirement, minimizing fees can have a profound impact on your nest egg. For short-term objectives, prioritizing performance over cost might be more appropriate.

Understanding Management Expense Ratios is crucial for making informed investment decisions. By carefully evaluating MERs and their impact on your portfolio, you can strike a balance between cost and performance, maximizing your returns over time. Always consult with a financial advisor to ensure your investments align with your goals and risk tolerance.

Key Takeaway: Knowledge is power. By being mindful of MERs and their role in investment performance, let Dunbrook Associates help you take a proactive approach to building wealth and achieving financial success.

Need Personalized Support?

Our team is committed to clarity, precision, and long-term guidance.

When building an investment portfolio, one of the most important decisions is whether to focus primarily on growth, income, or a combination of the two. Both growth investing and income investing can play a valuable role in a long-term financial plan, but they are designed to meet different needs.

Whether you're just beginning your financial journey or approaching retirement, developing strong financial habits today can significantly improve your financial future. The good news is that these habits don't require perfection they simply require consistency.

While an inheritance can provide financial security and new opportunities, making thoughtful decisions is essential to ensure those assets continue to benefit you and future generations.

July 13, 2026

Cookie Settings

We use cookies to enhance your browsing experience, serve personalised ads or content, and analyse our traffic. By clicking "Accept All", you consent to our use of cookies.