Salary or Dividends? Deciding How to Pay Yourself from a Corporation

Share

As a business owner or incorporated professional, one of the most crucial financial decisions you’ll face is determining how to pay yourself. Should you take a salary, dividends, or a combination of both? The right choice depends on your financial goals, tax situation, and long-term business strategy. This guide explores the key differences between salary and dividends, their advantages and disadvantages, and how to choose the best option for your circumstances.

Understanding Salary and Dividends

Before deciding how to structure your compensation, it’s important to understand how salaries and dividends work within a corporation and the implications on your tax planning.

Salary

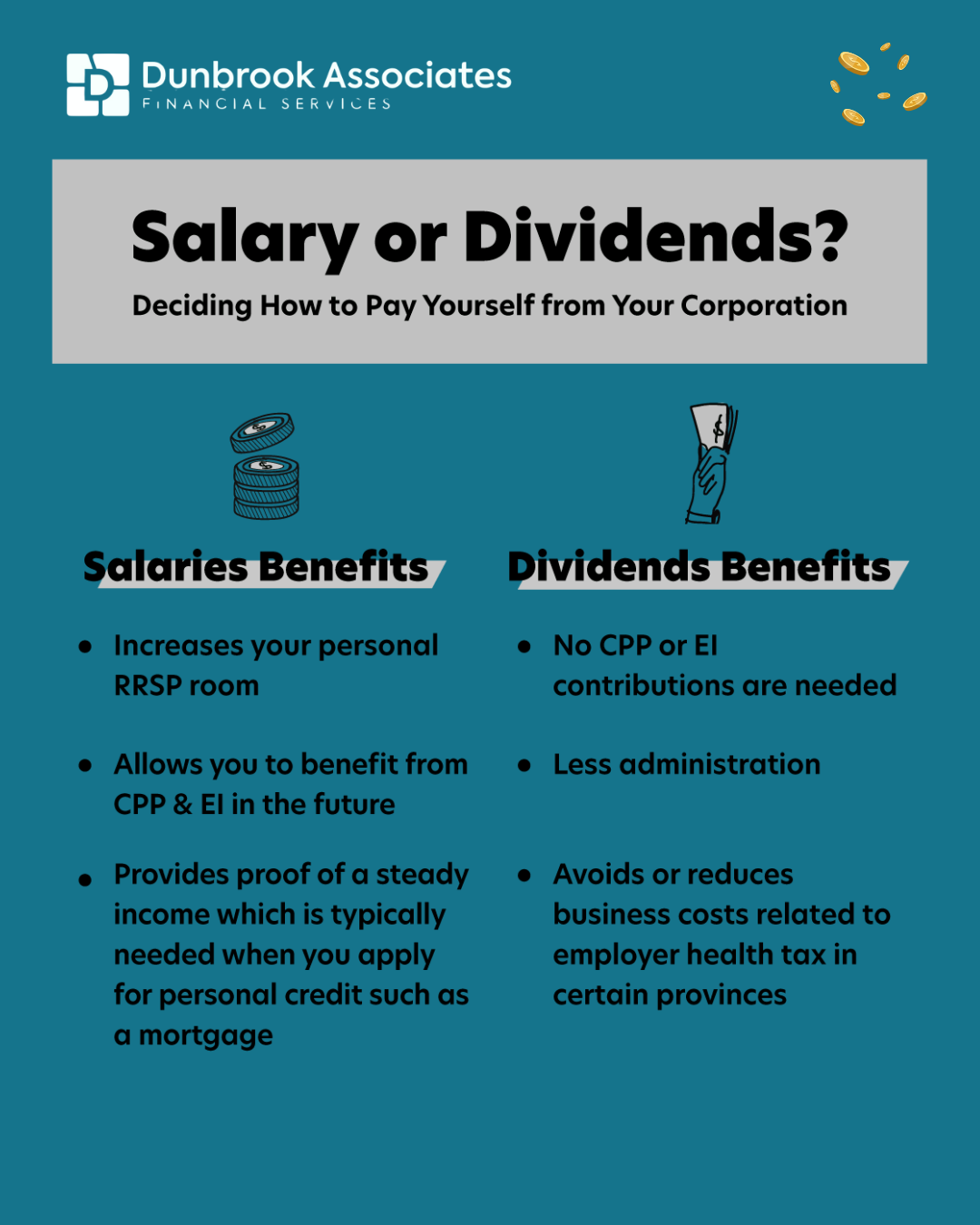

A salary is a regular paycheck that you receive from your corporation. It is considered earned income and is subject to payroll deductions, including Canada Pension Plan (CPP) contributions, Employment Insurance (EI) (if applicable), and income tax.

Dividends

Dividends are payments made to shareholders from the corporation’s after-tax profits. They are not considered earned income and are taxed differently from a salary. Since the corporation has already paid corporate tax on its profits, dividends are taxed at a lower rate at the personal level through the dividend tax credit.

Key Considerations When Choosing Between Salary and Dividends

Several factors influence whether a salary, dividends, or a mix of both is the best approach for you.

1. Tax Implications

The most significant consideration is tax efficiency.

Salary: Since salaries are deductible business expenses, they reduce the corporation’s taxable income. However, they are subject to personal income tax rates, which can be higher depending on your total earnings.

Dividends: While dividends are taxed at a lower rate due to the dividend tax credit, they are paid from after-tax corporate income. This means the corporation has already paid corporate tax before distributing dividends to shareholders.

2. Canada Pension Plan (CPP) Contributions

Salary: Paying yourself a salary means you contribute to CPP, which can help you build retirement benefits. However, both you and the corporation must contribute, which increases payroll costs.

Dividends: Since dividends are not considered earned income, they do not require CPP contributions. While this reduces your immediate expenses, it also means you will not accumulate CPP benefits for retirement.

3. RRSP Contribution Room

Salary: Salaries create Registered Retirement Savings Plan (RRSP) contribution room, allowing you to save more for retirement with tax-deferred growth.

Dividends: Since dividends are not considered earned income, they do not generate RRSP contribution room, potentially limiting your ability to save in tax-advantaged accounts.

4. Corporate Tax Rates vs. Personal Tax Rates

The tax advantages of dividends depend on the corporate tax rate in your province compared to your personal tax bracket. If your corporation is eligible for the small business deduction (SBD), it pays a lower tax rate on active business income, which can make dividends more attractive.

5. Income Smoothing and Cash Flow Considerations

Salary: Provides a predictable and stable income stream, which is beneficial for budgeting and personal financial planning.

Dividends: Can be paid out at any time based on available cash flow, offering flexibility. However, this means income may be inconsistent, which can make financial planning more challenging.

6. Eligibility for Personal and Corporate Deductions

Salary: Allows you to qualify for personal tax deductions such as childcare expenses and RRSP contributions.

Dividends: Since dividends do not qualify as earned income, they may not allow access to certain deductions and credits.

7. Employment Insurance (EI) Considerations

Salary: You may be eligible to contribute to EI, allowing you to receive benefits in the event of job loss or maternity leave.

Dividends: Do not contribute to EI, meaning you will not qualify for employment insurance benefits.

Pros and Cons of Each Approach

Salary Pros:

✔ Generates RRSP contribution room.

✔ Provides stable income for personal financial planning.

✔ Allows CPP contributions for future retirement benefits.

✔ Recognized as earned income for various tax deductions.

✔ Flexible payout structure based on business cash flow.

✔ No CPP contributions required, reducing payroll costs.

✔ Simpler to administer since no payroll deductions are needed.

Dividend Cons:

✖ Does not generate RRSP contribution room.

✖ No CPP contributions, affecting retirement benefits.

✖ Income may be irregular, making budgeting more difficult.

✖ Limited eligibility for certain personal tax deductions.

Finding the Right Balance: Salary vs. Dividends Hybrid Approach

For many business owners, a combination of salary and dividends provides the best of both worlds. This strategy allows you to:

Pay yourself a salary up to the RRSP contribution limit to maximize retirement savings.

Take dividends to take advantage of the lower dividend tax rate.

Minimize CPP contributions while ensuring some retirement benefits.

Optimize cash flow by adjusting dividends based on business performance.

Example Scenarios

Scenario 1: Maximizing RRSP Contributions

If you want to build retirement savings, paying yourself a salary of at least $75,000 (2024 RRSP limit threshold) will maximize your RRSP contribution room.

Scenario 2: Minimizing CPP Contributions

If you prefer not to contribute to CPP, you might take only dividends. However, you should have other retirement savings plans in place.

Scenario 3: Balancing Taxes and Benefits

If your corporation qualifies for the small business deduction, you could pay yourself a lower salary to contribute to CPP and RRSP, then supplement your income with dividends to take advantage of lower tax rates.

Choosing the Best Strategy for You

Deciding whether to take a salary, dividends, or a mix of both depends on your financial goals, tax situation, and retirement planning strategy. A tailored approach that considers corporate and personal tax implications can help optimize your income while ensuring financial stability. Consult with a financial advisor at Dunbrook Associates about your business planning needs and create a tax-efficient compensation plan that aligns with your business and personal financial goals.

Need Personalized Support?

Our team is committed to clarity, precision, and long-term guidance.

When building an investment portfolio, one of the most important decisions is whether to focus primarily on growth, income, or a combination of the two. Both growth investing and income investing can play a valuable role in a long-term financial plan, but they are designed to meet different needs.

Whether you're just beginning your financial journey or approaching retirement, developing strong financial habits today can significantly improve your financial future. The good news is that these habits don't require perfection they simply require consistency.

While an inheritance can provide financial security and new opportunities, making thoughtful decisions is essential to ensure those assets continue to benefit you and future generations.

July 13, 2026

Cookie Settings

We use cookies to enhance your browsing experience, serve personalised ads or content, and analyse our traffic. By clicking "Accept All", you consent to our use of cookies.