Permanent Life Insurance and Taxes: A Guide for Canadian Investors

Share

When planning your financial future, few tools are as versatile and impactful as permanent life insurance. Beyond providing lifelong coverage, permanent life insurance policies offer unique tax advantages that can benefit both you and your beneficiaries. In this guide, we will explore the intersection of permanent life insurance and taxes, helping you understand how this financial product can be a cornerstone of your wealth management strategy.

What is Permanent Life Insurance?

Permanent life insurance is a type of life insurance that provides coverage for your entire lifetime, as long as premiums are paid. Unlike term life insurance, which only covers a specific period, permanent life insurance includes a cash value component that grows over time. The two most common types of permanent life insurance are:

Whole Life Insurance: Offers consistent premiums, guaranteed death benefits, and a guaranteed rate of return on the cash value.

Universal Life Insurance: Provides flexibility in premium payments and death benefits, as well as options for investing the cash value in various portfolios.

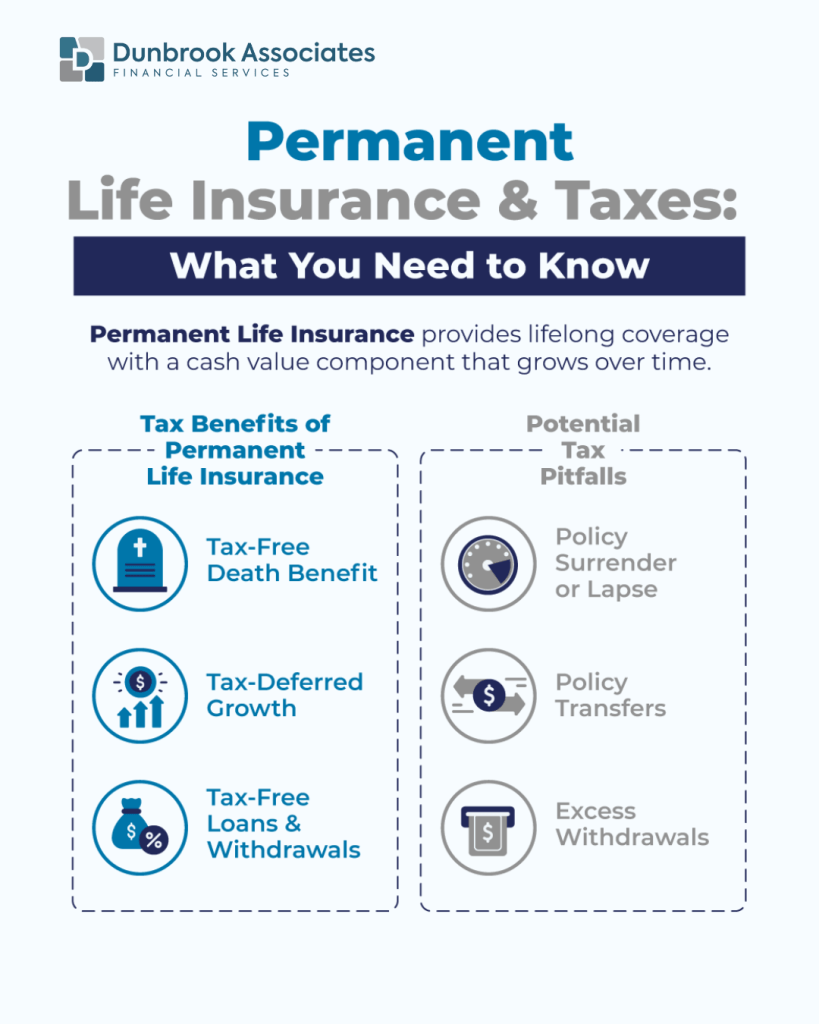

Tax Advantages of Permanent Life Insurance

One of the most compelling reasons to consider permanent life insurance is its tax benefits. Here are the key advantages:

1. Tax-Deferred Growth

The cash value within a permanent life insurance policy grows on a tax-deferred basis. This means you won’t pay taxes on the gains as long as they remain within the policy. Over time, this tax-deferred growth can significantly enhance the policy’s value.

2. Tax-Free Death Benefit

The death benefit paid to your beneficiaries is typically tax-free. This ensures that your loved ones receive the full amount of the benefit without any deductions for income taxes, making it an effective tool for estate planning.

3. Tax-Free Withdrawals and Loans

You can access the cash value of your policy through withdrawals or loans without incurring taxes, provided the amount does not exceed your policy’s adjusted cost basis. However, it’s important to structure these transactions carefully to avoid unintended tax consequences.

Using Permanent Life Insurance for Estate Planning

Permanent life insurance is a powerful tool for estate planning, particularly in addressing tax liabilities and preserving wealth for future generations. Here’s how it can help:

Minimizing Estate Taxes: Upon death, your estate may be subject to significant taxes, particularly if you own valuable assets such as real estate or investments. The tax-free death benefit from a life insurance policy can be used to cover these taxes, ensuring your heirs receive their intended inheritance.

Providing Liquidity: Many estates are asset-rich but cash-poor. Life insurance proceeds can provide the liquidity needed to settle debts, pay taxes, or support beneficiaries without requiring the sale of assets.

Preserving Wealth: By reducing the tax burden on your estate, permanent life insurance ensures that more of your wealth is passed on to your heirs.

Tax Implications of Premium Payments

While the benefits of permanent life insurance are substantial, it’s important to understand the tax implications of premium payments:

Personal Policies: Premiums paid for personal permanent life insurance policies are not tax-deductible.

Business-Owned Policies: If a business owns the policy and the coverage benefits the business, premiums may be deductible. However, this depends on the specific circumstances and should be reviewed with a financial advisor.

Corporate-Owned Life Insurance

For business owners, corporate-owned life insurance (COLI) can be a highly tax-efficient strategy. Here are some of its advantages:

Funding Buy-Sell Agreements: Life insurance can fund buy-sell agreements between business partners, ensuring a smooth transition of ownership.

Tax-Efficient Wealth Transfer: The death benefit can be paid into the corporation’s capital dividend account (CDA), allowing for tax-free distribution to shareholders.

Reducing Corporate Taxes: The cash value component grows tax-deferred, providing additional financial flexibility.

Potential Tax Pitfalls

While permanent life insurance offers many benefits, there are potential pitfalls to be aware of:

Exceeding Exempt Policy Limits: Policies must comply with maximum tax actuarial reserve (MTAR) limits to maintain their tax-advantaged status. Exceeding these limits can lead to the policy losing its tax-exempt status.

Policy Surrender or Cash Withdrawals: Surrendering a policy or withdrawing cash above the adjusted cost basis can trigger taxable income.

Policy Lapse: If loans or withdrawals exceed the cash value and the policy lapses, the outstanding amount may become taxable.

Strategies for Maximizing Tax Benefits

1. Pairing with a Retirement Plan

Permanent life insurance can supplement your retirement income by allowing tax-free withdrawals or loans from the policy’s cash value. This can be particularly valuable if you’ve maxed out other retirement savings options.

2. Leveraging Insurance for Charitable Giving

Donating a life insurance policy to a registered charity can provide you with tax credits while supporting a cause you care about. The charity can also benefit from a significant death benefit.

3. Utilizing the Capital Dividend Account (CDA)

For business owners, the CDA allows tax-free distribution of life insurance proceeds to shareholders. This can be a key strategy for transferring wealth tax-efficiently.

Who Should Consider Permanent Life Insurance?

Permanent life insurance is not a one-size-fits-all solution, but it is particularly beneficial for:

High-Net-Worth Individuals: Those with significant assets who need a tool for estate preservation and tax planning.

Business Owners: Individuals seeking tax-efficient ways to fund business transitions or protect their company.

Those with Long-Term Financial Goals: People who want a reliable, tax-advantaged vehicle for building and preserving wealth.

Consulting a Financial Advisor

Given the complexity of permanent life insurance and its tax implications, consulting a financial advisor is essential. An experienced advisor can help you:

Select the right type of policy for your needs.

Structure the policy to maximize tax benefits.

Integrate life insurance into your broader financial and estate planning strategy.

Dunbrook Financial Advisors specialize in tailoring life insurance solutions to meet your unique financial goals. Whether you’re looking to protect your family, grow your wealth, or plan your estate, we’re here to guide you every step of the way.

Permanent life insurance is more than just a safety net; it’s a versatile financial tool with significant tax advantages. From tax-deferred growth and tax-free death benefits to estate planning and corporate strategies, permanent life insurance can play a pivotal role in securing your financial future. To explore how permanent life insurance fits into your financial plan, contact Dunbrook Financial Advisors today.

Need Personalized Support?

Our team is committed to clarity, precision, and long-term guidance.

When building an investment portfolio, one of the most important decisions is whether to focus primarily on growth, income, or a combination of the two. Both growth investing and income investing can play a valuable role in a long-term financial plan, but they are designed to meet different needs.

Whether you're just beginning your financial journey or approaching retirement, developing strong financial habits today can significantly improve your financial future. The good news is that these habits don't require perfection they simply require consistency.

While an inheritance can provide financial security and new opportunities, making thoughtful decisions is essential to ensure those assets continue to benefit you and future generations.

July 13, 2026

Cookie Settings

We use cookies to enhance your browsing experience, serve personalised ads or content, and analyse our traffic. By clicking "Accept All", you consent to our use of cookies.