Mortgage Life Insurance vs. Personal Life Insurance: Which One is Right for You?

Share

When purchasing a home, one of the biggest financial commitments you'll make is securing a mortgage. To protect against unforeseen circumstances, many homeowners consider mortgage life insurance or personal life insurance. While both options offer financial protection, they serve different purposes and have distinct advantages and drawbacks. Understanding the key differences between mortgage life insurance and personal life insurance can help you make an informed decision that best suits your needs.

What is Mortgage Life Insurance?

Mortgage life insurance is a type of insurance specifically designed to pay off the remaining balance of your mortgage if you pass away. It ensures that your loved ones won’t have to worry about making mortgage payments after your death. This type of policy is usually offered by lenders and banks when you take out a mortgage loan.

Key Features of Mortgage Life Insurance

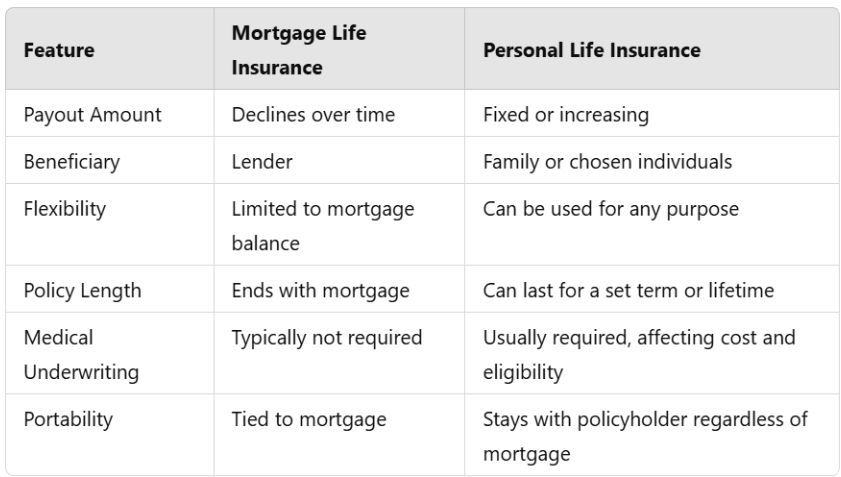

Declining Benefit – The payout decreases over time as the mortgage balance decreases.

Lender is the Beneficiary – The insurance payout goes directly to the mortgage lender, not your family.

Tied to Your Mortgage – Coverage ends when your mortgage is fully paid off or refinanced.

No Flexibility – The policy cannot be transferred to another property or used for other financial needs.

Pros of Mortgage Life Insurance

Ensures Mortgage Protection – Your family won’t have to worry about losing their home if you pass away.

Easy Approval Process – Often requires minimal or no medical underwriting, making it accessible to individuals with pre-existing health conditions.

Premiums Included in Mortgage Payments – Some lenders offer the convenience of bundling insurance premiums with mortgage payments.

Cons of Mortgage Life Insurance

Declining Coverage – The payout amount decreases as your mortgage balance reduces, but your premiums remain the same.

Limited Control – The payout only covers the mortgage and cannot be used for other financial needs.

Potentially Higher Cost – Compared to personal life insurance, mortgage life insurance may have higher premiums for the coverage provided.

What is Personal Life Insurance?

Personal life insurance is a policy that pays out a lump sum to your chosen beneficiaries upon your death. This insurance can be used for any purpose, including covering mortgage payments, daily living expenses, education costs, or other debts.

Types of Personal Life Insurance

Term Life Insurance – Provides coverage for a specific period (e.g., 10, 20, or 30 years). If you pass away during the term, your beneficiaries receive a lump sum payment.

Permanent Life Insurance – Includes whole life and universal life insurance, offering lifelong coverage with a cash value component that grows over time.

Key Features of Personal Life Insurance

Fixed or Increasing Benefit – Unlike mortgage life insurance, the payout remains the same or may increase over time.

You Choose the Beneficiary – Your family or loved ones receive the payout and can use it as needed.

Flexible Coverage – The policy is not tied to a mortgage and can cover multiple financial obligations.

Pros of Personal Life Insurance

Comprehensive Coverage – Can be used for mortgage payments, funeral expenses, debts, and other financial needs.

Flexibility – Beneficiaries have control over how they use the payout.

Potentially More Affordable – Depending on age and health, term life insurance may provide more coverage for a lower cost than mortgage life insurance.

Portable Policy – Coverage remains in place regardless of mortgage status or property ownership.

Cons of Personal Life Insurance

Medical Underwriting Required – Approval may depend on health factors, and higher-risk individuals may face higher premiums or coverage denials.

Premium Variability – Premiums may increase for permanent policies if not structured properly.

Requires Financial Planning – Beneficiaries need to allocate funds wisely to cover financial obligations.

Mortgage Life Insurance vs. Personal Life Insurance: Key Differences

Which One Should You Choose?

When to Choose Mortgage Life Insurance

You have difficulty qualifying for personal life insurance due to health issues.

You only want coverage for your mortgage and do not need additional life insurance protection.

You prefer the convenience of bundling insurance premiums with your mortgage payments.

When to Choose Personal Life Insurance

You want flexibility in how the payout is used (e.g., mortgage payments, debts, education, or living expenses).

You seek long-term coverage beyond your mortgage term.

You prefer to leave a financial safety net for your family rather than just covering the mortgage balance.

You are in good health and can qualify for a more affordable term life insurance policy.

While both mortgage life insurance and personal life insurance provide financial protection, personal life insurance offers greater flexibility, control, and value for your money. Mortgage life insurance may be a suitable option for those who cannot qualify for personal life insurance or prefer a simple, automatic way to ensure their mortgage is covered.

Before making a decision, assess your financial needs, health status, and long-term goals. Consulting a financial advisor at Dunbrook Associates can help you determine the best insurance strategy to secure your family's financial future while protecting your home investment.

Need Personalized Support?

Our team is committed to clarity, precision, and long-term guidance.

When building an investment portfolio, one of the most important decisions is whether to focus primarily on growth, income, or a combination of the two. Both growth investing and income investing can play a valuable role in a long-term financial plan, but they are designed to meet different needs.

Whether you're just beginning your financial journey or approaching retirement, developing strong financial habits today can significantly improve your financial future. The good news is that these habits don't require perfection they simply require consistency.

While an inheritance can provide financial security and new opportunities, making thoughtful decisions is essential to ensure those assets continue to benefit you and future generations.

July 13, 2026

Cookie Settings

We use cookies to enhance your browsing experience, serve personalised ads or content, and analyse our traffic. By clicking "Accept All", you consent to our use of cookies.